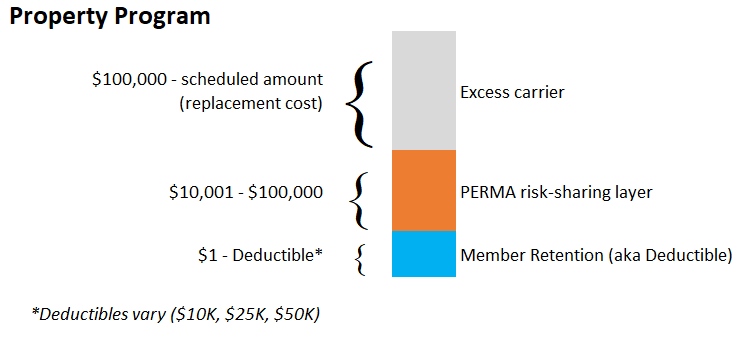

Property

PERMA group purchases commercial insurance for property, boiler & machinery, and pollution coverage on an All-Risk basis for property valued at approximately $3 billion. The program provides replacement cost coverage and a $300,000,000 “All-Risk” limit and a $100,000 pool deductible (inclusive of member deductible). Member deductibles are $10,000, $25,000, or $50,000. Minimal flood coverage (up to $10 million), except Flood Zones A & V which are not covered, is subject to a $100,000 deductible. Earthquake coverage is purchased separately on selected sites. For applicable Pollution coverage deductibles see policy. If you have any questions contact PERMA at info@permarisk.gov.

Boiler & Machinery

The PERMA property program includes equipment breakdown/boiler & machinery protection for perils normally excluded under a property policy such as power surges, short circuits, mechanical breakdown and boiler overheating or cracking. This extends coverage to electrical systems, HVAC, refrigeration units, pressure vessels, computers and communications equipment, mechanical equipment, and similar risks. The program also provides for jurisdictional inspections as required by law. Cal-OSHA requires inspections on the following types of equipment commonly found at PERMA member agencies: air tanks, LPG propane storage tanks over 125 gallons, and high pressure boilers over 15 psig steam (these could be boilers, water heaters, air compressors, natural gas tanks and petroleum tanks). To schedule a free jurisdictional inspection (because your agency participates in PERMA’s property program), please follow the instructions on the flyer.

Infrared Testing

An infrared thermographic electrical inspection provides information on the condition of electrical equipment. Faulty assembly/installation, loose connections, phase imbalance, overloaded circuits, faulty breakers, corrosion, and normal wear can be detected through infrared testing. If undetected, these electrical issues can result in thousands of dollars in costly repairs, downtime, and dangerous failures resulting in fires and explosions. The property program offers free infrared testing services to the members. If your agency participates in PERMA’s Property Program, you can schedule one day of testing at your facility. This service is offered at no cost, on a first come, first served basis. There is a limit on the number of service days available, so contact Kristi Loiselle at kloiselle@alliant.com or at (949) 260-5042 to schedule.

Online – Property Schedule Updates

Members are asked to schedule property upon acquisition if coverage is desired. PERMA members are able to update property schedules throughout the year through an online system – “InsureID.” Members were provided with login information and passwords. Any updates to the property and vehicle schedule, including additions and deletions, can easily be made online. Members are then able to receive real-time schedule adjustments and confirmation of the change(s). If a staff member at your agency needs access to make updates, please contact PERMA to have them added to the system.

- Buy something? Ensure it is listed so your agency has coverage.

- Sell something? Remove it from the schedule so your agency isn’t paying unnecessary premium.

- Is the COPE information complete? Carriers assume the worst, so your agency could be paying more if this information is missing. Construction Occupancy Protection Exposure (COPE) is a set of risks that property insurance underwriters review. COPE allows the insurer to evaluate the risks of insuring a piece of real estate, which will ultimately determine the ability to insure and if so, the cost of insurance

- Construction: Frame, masonry, masonry veneer, superior construction, mixed masonry/frame

- Occupancy: How the building is being used for commercial property, & whether it is owner-occupant or renter-occupied for homes, & the number of families for which the building is designed

- Protection: Quality of the responding fire department (paid/volunteer), adequacy of water pressure & water supply in the community, distance to the structure to the nearest fire station, quality of the hire hydrant, and distance of the structure to the nearest hydrant

- Exposure: Risk of loss posed by neighboring property of the surrounding area, taking into consideration what is located near the property, such as an office building, subdivision, or fireworks factory (source: https://www.irmi.com/term/insurance-definitions/cope)

Remember – your agency’s coverage and premium is determined by what you schedule.

Important update regarding contractor and mobile equipment:

Please note contractor and mobile equipment should be scheduled under the property program, unless it is licensed for road use. If the equipment is subject to vehicle registration based upon the California Vehicle Code (i.e. licensed for road use), then it should be scheduled on your agency’s vehicle schedule.

- While your agency can use one line item to list the value of contractor’s equipment or mobile equipment that is contained on one site, staff recommends you list the items individually on your schedule to ensure the values are appropriate and there are no coverage issues.

There is a distinction between mobile equipment vs. contractor’s equipment.

- Contractor’s equipment is only used for building/construction, while mobile equipment does not apply to those functions (i.e. a projector can be considered mobile equipment while it wouldn’t be considered contractor’s equipment).

- Note: heavy equipment is a subset of contractor’s equipment. Again, if the heavy equipment does not have motor vehicle registration, then it would be reported on the property schedule.

Tutorials to update your schedule are located at the links below along with a training video. If you encounter issues, or would like additional training, please contact Katie Achterberg. PERMA members are asked to make schedule updates throughout the year, as property and vehicles change, to ensure the annual renewal submissions are accurate.

Building and content values are updated annually based upon either appraisals or a trend factor selected by the carrier. As part of their membership, PERMA members receive field appraisals approximately every 4-5 years to ensure values remain appropriate.

Renovations & New Construction

Members that participate in the PERMA property program have a fantastic benefit: automatic Builder’s Risk coverage (aka Course of Construction) when renovations take place on existing buildings. This coverage, for renovation and remodel work within the four walls of any existing building on the Schedule, is included at no additional premium. If you have these types of projects, the contractor should NOT be required to provide Builder’s Risk / Course of Construction coverage within their proposal bid. When construction has been completed, remember to evaluate the building value on the Schedule to ensure it is reflective of the work that was completed.

If your agency is adding new square footage or additions to existing scheduled buildings, the property program also has built in coverage is as follows:

- The property program will provide Builder’s Risk coverage for new square footage/additions projects, up to $15M in hard costs, at no premium due during the current policy term. If the project work extends past the current policy term, premium is collected at that next July 1st renewal date.

- Any project above $15M in hard costs/construction costs, the property program carriers need to underwrite the project and quote with additional premium during the current policy term.

- A form must be completed for any project adding new square footage/additions or new construction. The coverage is very broad, and the limit is purchased based on the individual project.

For more information, please contact PERMA's broker Matt McManus.

Report a Loss

Effective January 1, 2026, PERMA staff began handling member's property claim in-house. Members are responsible for the following:

- Timely and accurate claim reporting.

- Report the loss, using the Property Loss Notification Form, as soon as possible but within 30 days.

- Do not wait for a police report, repair estimate, or other documentation.

- All claims must be reported, including claims with a value anticipated to be below the member deductible.

PERMA staff will report losses to excess carriers as necessary. According to the policy, notice is to be made as soon as practicable, upon knowledge within the risk management or finance division of the insured, that a loss has occurred. The carrier clarified that reporting the loss within 30 days will meet the “as soon as practicable” requirement for initial loss reporting.

Pollution Claims Reporting

Pollution policies are written on a “Claims Made and Reported” coverage form which means that all claims and known incidents that could give rise to a claim must be reported to the Insurer during the policy period in order for coverage to apply. Below is the definition of a “CLAIM” according to Ironshore Specialty Insurance Company. Please review this definition carefully to understand what should be reported:

Claim means a written demand, notice or assertion of a legal right alleging liability or responsibility on the part of the Insured.

In order to automatically preclude known incidents from being considered for coverage due to late reporting, anything that fits within the definition of “CLAIM” needs to be reported to Ironshore Specialty Insurance Company by June 30, 2025. We strongly recommend that you check with anyone in your entity that may know of or have knowledge of a “CLAIM.” There is no penalty for reporting any claim or known incident. Please report any incidents that could possibly give rise to a pollution claim to the following contacts:

If you have questions about the Pollution and Remediation Legal Liability policy or reporting claims, please contact:

Ironshore Environmental Claims CSO

28 Liberty Street, 5th Floor

New York, NY 10005

In emergency call: (888) 292-0249

Fax: (646) 826-6601

Email: USClaims@ironshore.com

Akbar Sharif

Claims Advocate

18100 Von Karman Avenue, 10th Floor

Irvine, CA 92612

Voice: (949) 260-5088 Fax: (415) 403-1466

Email: akbar.sharif@alliant.com

Drone Coverage

If your agency has a drone, please be aware that your agency has liability coverage related to the drone, however, it will need to be added to your agency’s property schedule to have physical damage coverage while the drone is not in use. Your agency needs to complete a separate application if it wishes to insure the drone for physical damage coverage when it is in use.

Liability Coverage:

- While aircraft are excluded from PERMA’s memorandum of coverage (MOC), the definition of aircraft does not include unmanned aircraft (aka drones). See sidebar for the applicable MOC.

- In other words, while coverage for each claim is determined based upon the merits of the claim, the members’ intent is to include drones in the liability coverage.

- PRISM’s MOC is similar – the aircraft exclusion does not apply to unmanned aerial vehicles (UAV) owned or operated by or on behalf of, or rented to, or loaded by any covered party.

Property Coverage:

- While in storage: The property program provides physical damage coverage while the drone is being stored.

- To trigger this coverage, the drone must be added to the City’s property schedule as “contents.”

- While in flight: The property program does not provide physical damage coverage while the drone is being flown.

- Some stand-alone policies offer both liability and physical damage coverage, however, as noted above your agency already has liability coverage, so it only needs physical damage coverage (if interested).

- The cost of coverage varies based upon the size/value/type of the drone.

General drone information:

- Your agency needs to ensure it is operating the drone in accordance with Federal Aviation Administration regulations, including registering it if it is over 55 pounds.

- The “Public Safety & Government” links on the FAA’s site also include tips on starting a drone program, understanding authority (this addresses third-parties using drones), and more.